Highlights

- Diplomatic Breakthrough: The announcement of preliminary “Peace Dividend” talks between Washington and Tehran has significantly reduced the geopolitical risk premium in global equities.

- Market Milestone: All three major U.S. indices surged to Wall Street record highs, with the S&P 500 crossing a historic psychological threshold as volatility (VIX) plummeted.

- Energy Deflation: Crude oil futures experienced their sharpest single-day decline of the year, easing inflation fears and providing the Federal Reserve with more room for potential rate cuts.

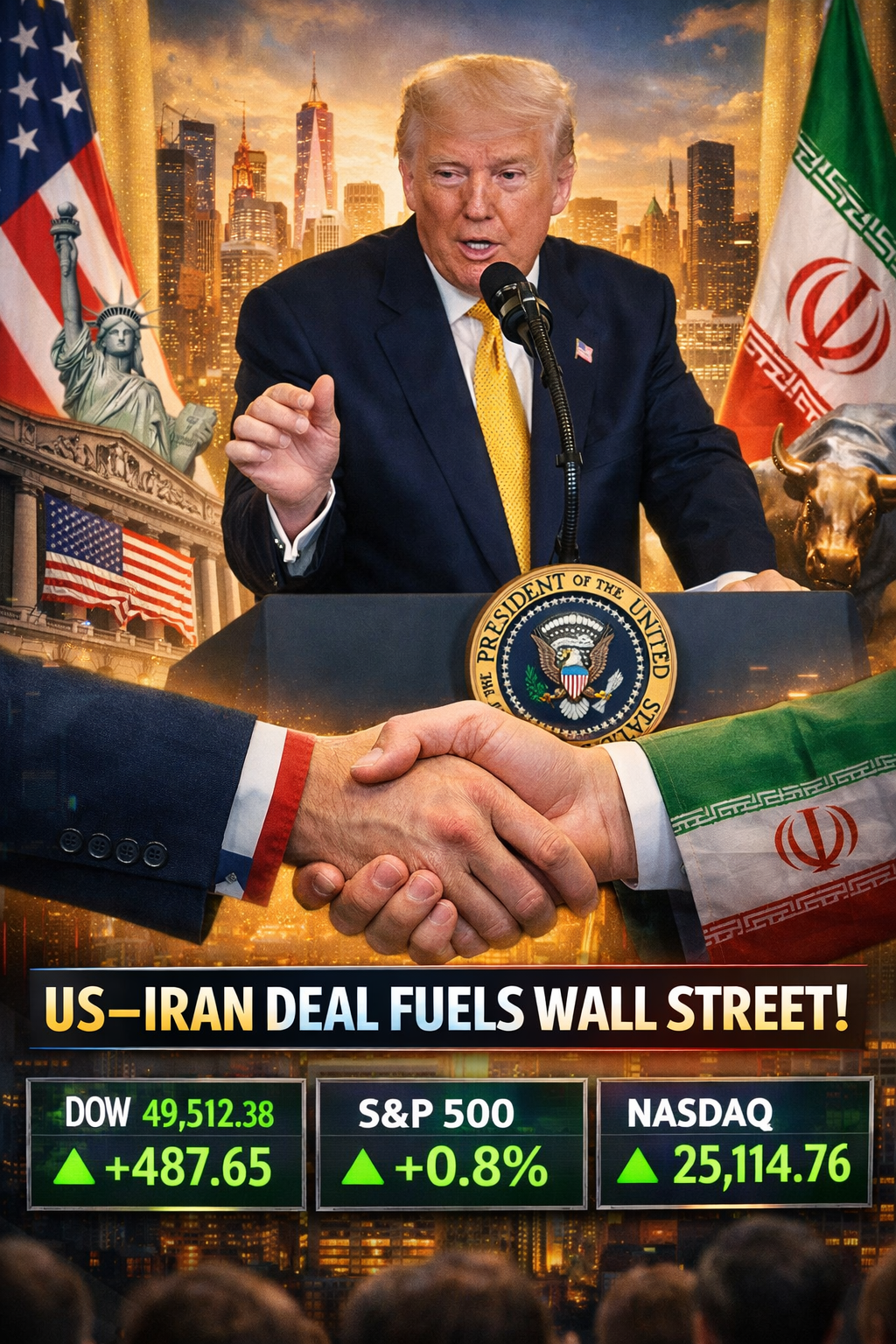

On May 7, 2026, the financial world witnessed what many are calling the “thaw of the decade.” Following months of back-channel diplomacy and rising tensions in the Middle East, the sudden announcement of formal negotiations between the United States and Iran has sent a shockwave of optimism through global trading floors. The immediate result was a frantic buying spree that lifted Wall Street record highs to levels previously thought unattainable in the current fiscal year. For investors who spent much of early 2026 bracing for “sticky” inflation and high-energy costs, the prospect of a stabilized Strait of Hormuz is acting as a massive liquidity injection into the global economy.

The Dow Jones Industrial Average soared more than 900 points in a single session, while the Nasdaq Composite, heavily weighted toward tech firms reliant on stable global supply chains, jumped 3.8%. This rally is not merely a reflexive bounce; it is a fundamental repricing of risk. When the risk of a regional conflict that could choke off 20% of the world’s oil supply begins to recede, the discount rates applied to future corporate earnings undergo a massive downward revision. Consequently, we are seeing a “melt-up” in equity valuations that is pulling sidelined capital back into the market at a record pace.

Anatomy of a Market Surge: Why Investors are Buying the “Big Thaw”

The mechanics behind the current Wall Street record highs are multi-faceted. First and foremost is the impact on energy. Energy prices have been the primary “inflation dragon” that central banks have struggled to slay. With the U.S. and Iran discussing a phased lifting of sanctions in exchange for verified nuclear and regional concessions, the market is already pricing in an influx of Iranian crude into the global market. Brent crude, which had been hovering near $95 per barrel, tumbled toward $78 in a matter of hours. This “energy tax cut” for the global consumer is expected to bolster retail spending and reduce manufacturing overheads, particularly in energy-intensive sectors like automobiles and heavy industry.

Furthermore, the technology sector is benefiting from a renewed sense of security regarding global trade routes. As semiconductor firms continue their aggressive expansion into AI infrastructure, the stability of maritime logistics is paramount. A peaceful resolution in the Middle East ensures that the critical shipping lanes connecting European markets with Asian manufacturing hubs remain unhindered. This geopolitical de-escalation is providing the perfect backdrop for the “Agentic AI” revolution, as companies feel more confident in committing to long-term, multi-billion dollar infrastructure projects without the looming shadow of a global energy crisis.

Geopolitical Ripple Effects: From the Strait of Hormuz to Silicon Valley

The implications of this diplomatic breakthrough extend far beyond the ticker tapes of Lower Manhattan, where Wall Street record highs have already signaled renewed investor optimism. In Europe, the DAX and CAC 40 indices posted their best gains since 2024, as the Eurozone stands to be one of the largest beneficiaries of lower natural gas and oil prices. The “peace dividend” is effectively a global stimulus package that doesn’t require government spending or debt issuance. Instead, it is a restoration of market confidence that allows the “invisible hand” to allocate capital toward growth rather than hedging against catastrophe.

In Asia, the news has complemented the already bullish sentiment found in Tokyo and Mumbai. As the Nikkei remains at elevated levels, the prospect of a stable U.S. dollar and lower energy costs is viewed as a net positive for Japanese exporters. Meanwhile, in India, the Nifty 50 is seeing a resurgence in foreign institutional investment (FII) as the global “risk-on” appetite grows. Investors are shifting away from defensive postures selling off gold and long-dated government bonds to chase growth in emerging markets and high-growth tech stocks.

The Fed’s New Dilemma: Balancing Growth and Exuberance

While Wall Street record highs are a cause for celebration among retail and institutional investors alike, they present a complex puzzle for the Federal Reserve. Chairman Jerome Powell and the Board of Governors must now determine if this rally is a sustainable reflection of improved macro conditions or the beginning of a speculative bubble. With energy-led inflation subsiding, the case for a series of interest rate cuts in the second half of 2026 has strengthened significantly. However, the Fed remains wary of “irrational exuberance.”

If the U.S.-Iran talks lead to a permanent treaty, the structural shift in the global economy would be disinflationary. This would allow the Fed to normalize rates toward a “neutral” level of 3% or 3.5%, a far cry from the restrictive levels seen over the past two years. Market participants are already betting on a 25-basis point cut as early as the June meeting, a sentiment that is further fueling the current equity rally. The core of the argument is simple: if the geopolitical “dark clouds” are clearing, the premium on cash can finally be lowered in favor of productive assets.

Sectoral Winners in the 2026 Rally

As we analyze the current record-breaking environment, certain sectors are standing out as clear leaders:

- Consumer Discretionary: With lower gas prices at the pump, American and European consumers are finding themselves with more disposable income, a trend reinforced by Wall Street record highs that signal renewed confidence in global markets. Retail giants and luxury brands are seeing a sharp uptick in forward guidance as they prepare for a robust summer spending season.

- Transportation and Logistics: Airlines, which have been battered by fluctuating fuel surcharges, are seeing their margins expand overnight. Major carriers have already begun announcing a reduction in “fuel recovery fees,” a move that is expected to drive a record-breaking year for international travel.

- Finance and Banking: Higher transaction volumes and a surge in IPO activity fueled by the stable market environment are boosting the bottom lines of investment banks. The “deal-making” drought of 2025 appears to be officially over as corporations rush to the public markets to capitalize on high valuations.

Conclusion

The path to these Wall Street record highs has been anything but linear. It has been a journey marked by resilience in the face of conflict, innovation in the face of stagnation, and now, diplomacy in the face of discord. The US-Iran deal talks represent more than just a political maneuver; they are a catalyst for a global economic reset. While the negotiations are still in their preliminary stages, the market’s reaction is a clear signal that the world is hungry for stability.

As we look toward the remainder of 2026, the focus will remain on the “execution” of this peace. Any setbacks in the talks could lead to sharp pullbacks, but the current momentum suggests that a new floor has been established for the global markets. For the first time in years, the primary driver of the news cycle is not a new crisis, but the potential resolution of an old one. In the world of finance, that is perhaps the most bullish indicator of all.

Visit Augmenting Money for the most recent information.

Leave a Reply